Everyone's Asking About AI

Commentary • Education

Date posted

May 14, 2026

Here's What We Actually Think

Barely a week goes by without a client asking some version of the same question: are we missing out on AI?

It's a fair question. The numbers coming out of the AI sector are genuinely hard to ignore. On March 31, 2026, OpenAI closed a $122 billion funding round, the largest private capital raise in history, at a valuation of $852 billion. The investors backing it include Amazon, Nvidia, SoftBank, Andreessen Horowitz, and Sequoia. These are some of the most sophisticated and well-resourced investors in private markets anywhere in the world. But here's what we've learned from watching institutional capital move for a long time: the headline is rarely the most interesting part of the deal.

What the OpenAI Round Actually Looks Like Up Close

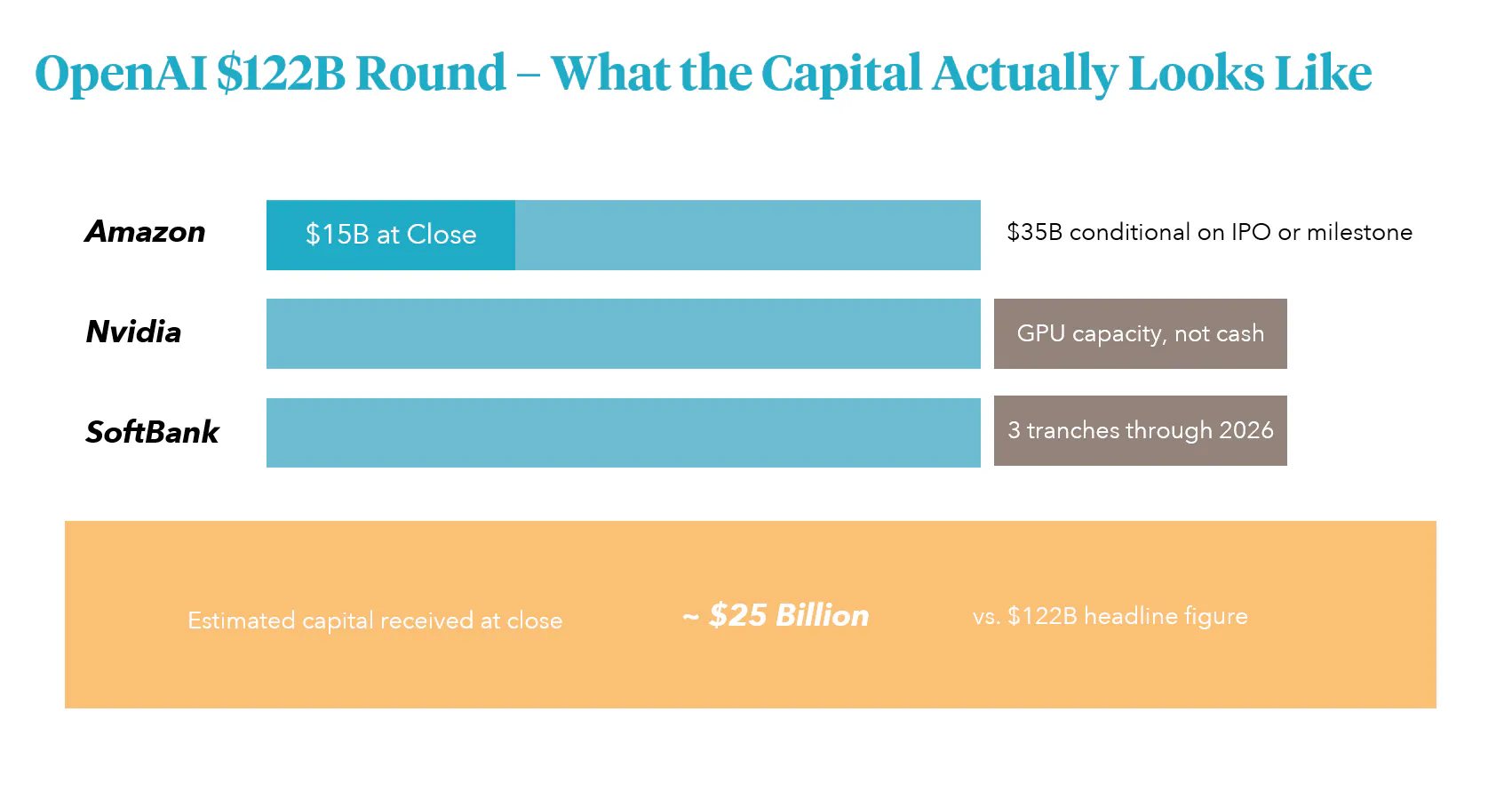

When you look past the $122 billion number, the structure of this round tells a different story than the one in the news. [1]

Image 1: OpenAI Series F funding round structure, March 2026. Sources: Bloomberg, Financial Times.

Amazon committed $50 billion, but $35 billion of that only flows if OpenAI completes an IPO or reaches a specific AI capability milestone. Nvidia's $30 billion contribution is largely in dedicated GPU capacity, not cash. SoftBank's $30 billion arrives in three equal tranches across 2026. When you add it up, OpenAI received roughly $25 billion in actual immediate capital at close, not $122 billion.

None of this is a criticism. This is how sophisticated investors manage risk when they're writing very large cheques into very uncertain situations. They build in conditions. They tie capital to milestones. They take their returns in forms other than cash. The structure is the point. What it tells us is that even the most bullish, deep-pocketed institutions in the world are not simply wiring money to OpenAI and hoping for the best. They are deploying capital carefully, conditionally, and with specific protections built in.

What Does This Mean For You?

The question clients are really asking isn't "should we own OpenAI." It's broader than that: should we have more exposure to AI as a theme? Are we positioned to benefit if this technology is as transformative as people say? Our honest answer has a few parts.

First, AI is already in your portfolio. Many of the private equity and infrastructure funds we allocate to are actively deploying AI tools to improve the businesses they own, reducing costs, improving margins, and accelerating value creation. You don't need a direct position in an AI company to benefit from what the technology is doing to private markets broadly. [4]

Second, direct exposure to AI companies is genuinely hard to access well. The best opportunities are private, early, and heavily oversubscribed. When access does exist through secondary markets, the terms are often buried in layers of conditions, contingent payouts, lockup periods, and payout hierarchies that determine who gets paid first if things don't go as planned. Miss those details and you can end up owning something that looks very different from what you thought you bought. That said, we have been deliberate about building selective exposure where the terms make sense, including positions in some of the most sought-after names in AI, among them OpenAI and Anthropic. [5]

Third, the discipline matters more than the theme. The investors who tend to do well in cycles like this are not the ones who moved fastest. They are the ones who evaluated each opportunity the same way they evaluate everything else: what's the structure, who has control, what's the time horizon, and what's the downside if things don't go as planned.

Where We Stand

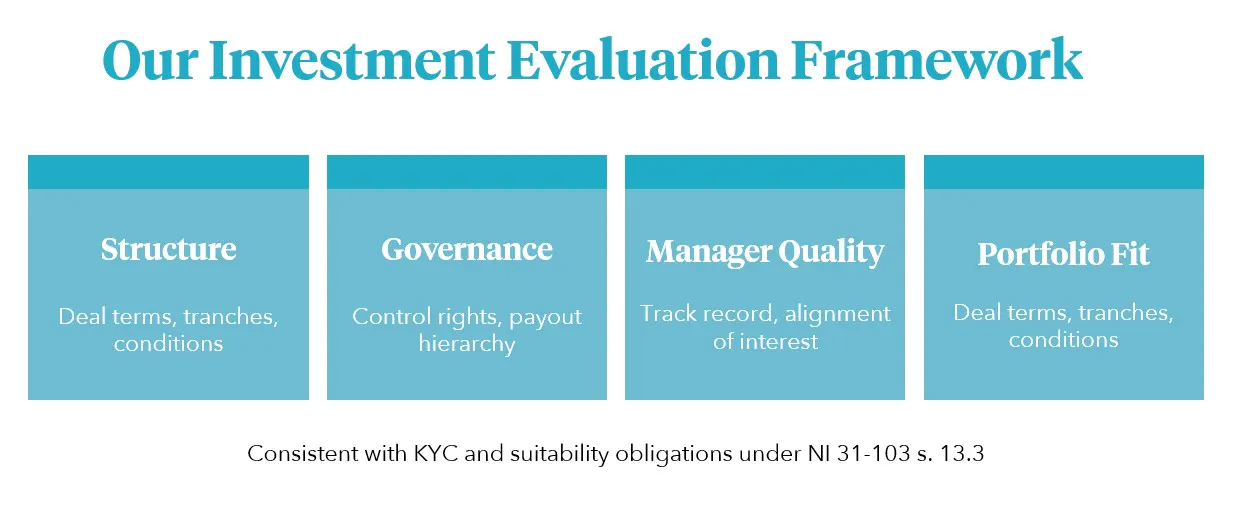

We are not avoiding AI. We are evaluating it — the same way we evaluate every private markets opportunity, on the basis of structure, governance, manager quality, and fit within the broader portfolio.

Some of what we see in the AI space meets that bar. A lot of it doesn't, at least not at current valuations and with current deal terms. That's not a cautious view of the technology, it's a disciplined view of the investment. If you're wondering whether your portfolio is positioned well for what AI is doing to the economy over the next decade, that's exactly the right conversation to be having. It just starts with the structure, not the headline.

Disclaimer

This communication is prepared by Kinsted Wealth, it is registered as a Portfolio Manager in Alberta, British Columbia, Saskatchewan, Ontario, Manitoba, Quebec, Nova Scotia, and Yukon, and as an Investment Fund Manager and Exempt Market Dealer in Alberta and Ontario under National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (eff. January 1, 2026). It is intended for informational purposes only and does not constitute personalised investment advice or a recommendation to buy or sell any security. Investment in private markets, including AI-related securities, involves significant risk, including potential loss of principal, limited liquidity, and exposure to complex deal structures. Investments in exempt market securities are available only to eligible investors as defined under NI 45-106 Prospectus Exemptions. This publication is not a prospectus. Past positioning in specific securities is not indicative of future opportunities or performance. Please refer to your Relationship Disclosure Information document or contact your advisor for information specific to your circumstances.

Sources and Regulatory Disclosures

[1] OpenAI Series F funding round structure — Bloomberg and Financial Times, March–April 2026 reporting on investor commitments, tranche conditions, and capital at close.

[2] NI 45-102 — Resale of Securities, Alberta Securities Commission. Governs hold periods and resale restrictions applicable to exempt market securities, including secondary market positions in private AI companies.

[3] ASC NI 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (consolidated, eff. Jan 1, 2026). ss. 13.2 (KYC), 13.3 (suitability), 13.4 (conflicts of interest), 14.2 (relationship disclosure). asc.ca

The views below reflect our general investment philosophy and are not a personalised suitability

determination for any individual client. Suitability varies by client objectives, risk tolerance, time horizon, and financial circumstances. Please speak with your advisor for guidance specific to your portfolio.

[4] ASC NI 45-106 Prospectus Exemptions. Accredited investor and minimum amount exemptions applicable to private market offerings. asc.ca

Access to secondary market AI positions described below is available only to eligible investors as defined under NI 45-106 (e.g. accredited investors). Such securities are subject to resale restrictions under NI 45-102

[5] CSA Staff Notice 31-325 — Marketing Practices of Portfolio Managers (July 5, 2011, still in force). Governs accuracy, fairness, and completeness of client-facing marketing communications.

Reference to specific holdings (OpenAI, Anthropic) reflects past positioning by the firm and is not a recommendation to purchase these securities. Not all clients hold these positions.

Past access to specific opportunities is not indicative of future availability or performance.

[6] CSA Staff Notice 31-363 — Client Focused Reforms: Review of Conflicts of Interest Practices (Aug 3, 2023). Guidance on disclosure when holding proprietary positions.

Regards,

Kinsted Wealth