What Today's Market Volatility Really Means for Long-Term Investors

Commentary • Education

Date posted

Apr 15, 2026

What Today's Market Volatility Really Means for Long-Term Investors

Market headlines are loud right now. Trade disputes, geopolitical tension, stubborn inflation, rapid AI adoption, and political uncertainty continue to dominate the news cycle. In periods like this, it’s natural for investors to feel uneasy.

But seasoned wealth managers across Canada consistently see the same pattern repeat volatility itself is not what undermines long‑term outcomes, emotional reaction to volatility is. Whether you’re a business owner in Calgary, a professional nearing retirement in Toronto, or a family planning across generations in Vancouver, understanding what market volatility actually signals, and what it doesn’t, can meaningfully influence long‑term wealth outcomes.

What's Driving Market Volatility Right Now?

Today's turbulence isn't random. It reflects a convergence of structural and cyclical forces reshaping global markets:

- Trade policy uncertainty: U.S. tariffs on Canadian, Chinese, and Mexican goods have created persistent supply chain anxiety and dampened risk appetite globally. [1]

- Inflation pressures: RBC revised its 2025 U.S. core inflation forecast upward to approximately 2.9%, partly driven by tariff cost pass-throughs. [2]

- Slowing growth signals: Goldman Sachs cut its 2025 U.S. GDP growth forecast to 1.7%, down from 2.4%, citing trade drag and policy uncertainty. [1,3]

- AI-driven market concentration: Returns in 2025 were heavily concentrated in a narrow set of large-cap technology and AI-related names, leaving many other stocks flat or down. [2]

- Government debt and fiscal policy: Ballooning deficits across major economies are raising scrutiny from bond markets, putting upward pressure on long-term interest rates. [2]

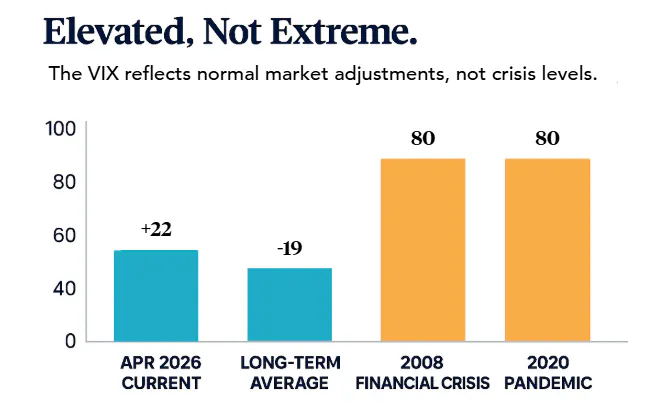

The CBOE Volatility Index (VIX), often called the market’s “fear gauge”, has moved modestly above long‑term averages. Importantly, it remains well below levels associated with true market crises such as 2008 or early 2020. Context matters. This looks far more like market adjustment than market collapse. [1,7]

Graph 1: CBOC, VIX Index. Long-term Average Since 1990

What History Actually Tells Us About Market Corrections

Here's the data point most investors need to hear more often: the S&P 500 has experienced 14 corrections since 1982, with average declines of 12%, and those corrections typically recovered within four months.1 The average one-year return following a market low was over 30%, jumping to more than 43% after two years. [1]

Even more striking is the cost of trying to sidestep volatility:

An investor who stayed fully invested from 2003 to 2022 earned approximately 9.8% annually. Missing just the 10 best days in that period cut returns nearly in half, to around 5.6% annually. [1] Critically, most of those best single-day gains occurred during the worst market periods, the 2008 crisis and the 2020 COVID crash. [1] Investors who fled to the sidelines missed the rebound entirely. The conclusion from decades of market data is consistent: time in the market beats timing the market.

The 3 Biggest Mistakes Long-Term Investors Make During Volatility

1. Selling Into the Decline

Panic selling locks in losses and forces you out of the market at exactly the wrong moment. According to Morningstar's "Mind the Gap" study, investors who attempted to time the market realized returns approximately 1.7% lower over the long term than those who stayed invested. [4,5] Over a 20 or 30-year horizon, that gap is enormous.

2. Abandoning a Diversified Strategy

When volatility hits, concentrated portfolios feel it hardest. Approximately 40% of S&P 500 companies declined in price in 2025, despite strong headline index returns, a clear demonstration of how narrow market leadership can mask significant underlying damage to undiversified portfolios. [2]

3. Assuming This Time Is Different

Every major bout of volatility comes packaged with a compelling narrative for why this downturn is uniquely dangerous. It rarely is. The fundamentals of long-term wealth building, diversification, consistent contribution, and disciplined rebalancing, have survived world wars, recessions, pandemics, and interest rate crises. They'll survive this too.

What Smart Canadian Investors Are Doing Right Now

Staying Invested and Rebalancing Strategically

Rather than retreating, disciplined investors are using this period to rebalance toward undervalued areas and away from overconcentration in last cycle's winners. With roughly 40% of S&P 500 companies having declined in 2025, fundamental analysis is becoming a more critical differentiator of performance in 2026. [2] At Kinsted, rebalancing decisions are systematic and evidence‑based, designed to reduce risk drift rather than chase short‑term performance, particularly when market leadership becomes unusually concentrated.

Broadening Into Private Markets

Private equity, private credit, and infrastructure investments have shown their worth as stabilizers. During the period from January 2022 to September 2024, a period of significant public market volatility, private equity returned +0.05%, private real estate +0.18%, and private debt +0.51%, buffering against sharp sentiment-driven swings in public markets.[1] For high-net-worth Canadians, access to private market allocations through a qualified wealth management firm is increasingly a standard portfolio consideration.

Cash Flow Matters, Especially Near Retirement

For portfolios approaching distribution phases, risk management increasingly becomes about cash flow, not just returns. Holding appropriate levels of liquidity, often one to three years of planned spending, allows portfolios to fund withdrawals without being forced to sell long‑term holdings during unfavourable market conditions. This structural feature removes one of the most common behavioural traps during downturns. [6]

Accumulation Portfolios and Volatility

In discretionary portfolios still in accumulation mode, regular contributions are invested systematically. As a result, periods of volatility naturally lead to lower average purchase prices over time, without requiring tactical decision‑making or emotional intervention. This mechanical feature of disciplined investing often works quietly in investors’ favour during market drawdowns. [6]

Tax Awareness During Market Dislocations

Volatile markets can also create opportunities for tax‑aware portfolio management, including tax‑loss harvesting and thoughtful rebalancing across registered and non‑registered accounts. Coordinating RRSP, TFSA, and taxable strategies during these periods can meaningfully improve after‑tax outcomes over time. [6]

Graph 2: JP Morgan "Guide to the Markets" (2023), S&P 500 Total Return. Annualized Returns.

The 2026 Outlook: Reasons for Measured Optimism

Despite the noise, the underlying fundamentals for long-term investors remain constructive:

- S&P 500 earnings growth is projected at approximately 13% for 2026, shifting markets into a fundamentals-led phase where profits, not multiple expansion, drive returns. [1,2]

- AI adoption continues to generate real productivity gains and capital expenditure across the economy, cascading benefits from semiconductor leaders to cloud platforms to enterprise software.

- Fiscal stimulus from major governments, including infrastructure and defence spending, is providing economic tailwinds even as monetary policy moderates.

- Emerging markets are attracting renewed interest as an alternative to expensive U.S. large-cap equities, supported by a stabilizing U.S. dollar. [1,2]

None of this eliminates risk. Persistent inflation, high government debt, labour market softness, and geopolitical flashpoints remain legitimate concerns. But for investors with a 10-, 20-, or 30-year horizon, the current environment looks far more like a speed bump than a structural break.

What This Means for Your Wealth Management Strategy in Canada

The most resilient strategies share a common thread: they were built for volatility before it arrived, the same philosophy that underpins Kinsted’s investment platform and long‑term planning approach.

That means:

- A clearly defined asset allocation matched to your actual risk tolerance and time horizon, not last year's risk tolerance

- Diversification across asset classes, including alternatives and private markets where appropriate

- A cash flow strategy that eliminates the need to sell equities at the worst time

- A tax-efficient structure across registered and non-registered accounts

- Regular reviews with a qualified advisor, not reactive calls driven by headlines

The investors who build wealth across market cycles aren't the ones who predicted the corrections. They're the ones who had a plan and stuck to it. At Kinsted, we design portfolios with the assumption that periods of volatility are inevitable, not exceptional. Rather than reacting to market stress as it arises, our investment platform is built in advance to manage it thoughtfully and consistently. That starts with globally diversified asset allocation, deliberately avoiding over‑reliance on any single market, sector, or theme, particularly during periods when returns become narrowly concentrated. Portfolio construction is paired with disciplined rebalancing, ensuring risk stays aligned with a client’s long‑term objectives rather than drifting with market sentiment.

Where appropriate, portfolios are complemented with private and alternative investments selected for diversification, income characteristics, and lower correlation to public markets, not as return enhancers, but as risk management tools within a broader plan. Just as importantly, investment strategies are integrated with tax‑aware structuring across registered and non‑registered accounts, recognizing that after‑tax outcomes, not headline returns, ultimately drive long‑term wealth.

Sources

[1] Harbourfront Wealth Management. (2025, March 21). Navigating current market turmoil.

https://www.harbourfrontwealth.com/2025/03/21/navigating-current-market-turmoil/

[2] RBC Wealth Management Canada. (2025). Navigating 2026: Strategic investing amid persistent volatility and market noise.

https://ca.rbcwealthmanagement.com/ascendant.wealth/blog/4710848-Navigating-2026-Strategic-Investing-Amid-Persistent-Volatility-and-Market-Noise

[3] Goldman Sachs Group, Inc. (2025). U.S. economic outlook and GDP growth revisions.

(Cited via Harbourfront Wealth Management.)

[4] Morningstar, Inc. (n.d.). Mind the Gap: The cost of investor timing.

(Cited via McBride Wealth Management.)

[5] McBride Wealth Management. (n.d.). Stick to your plan when markets get noisy.

https://www.mcbridewealthmanagement.ca/stick-to-your-plan-when-markets-get-noisy

[6] Griggers Wealth Management. (n.d.). Investment tips for investing in a volatile market.

https://griggerswealth.com/blog/investment-tips-for-investing-in-a-volatile-market/

[7] Chicago Board Options Exchange. (n.d.). CBOE Volatility Index (VIX).

(Referenced via Harbourfront Wealth Management analysis.)

Disclaimer: This commentary is provided for informational and educational purposes only and does not constitute investment, legal, tax, or other professional advice. The views expressed are current as of the date of publication and may change without notice.

This article may contain forward‑looking statements, including forecasts, projections, and assumptions about economic conditions, market performance, and investment outcomes. Forward‑looking statements are based on current expectations and assumptions and involve risks and uncertainties. Actual results may differ materially due to a variety of factors, including changes in market conditions, economic developments, interest rates, geopolitical events, and regulatory environments.

Historical market data and performance statistics are presented for illustrative purposes only and are not intended to represent the performance of any specific investment or client portfolio. Past performance is not indicative of future results. Market indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly.

References to asset allocation, rebalancing, private markets, or other investment strategies are general in nature and may not be suitable for all investors. Private and alternative investments involve additional risks, including limited liquidity, valuation uncertainty, longer investment horizons, and suitability requirements. Such investments are typically available only to investors who meet specific eligibility criteria.

This content does not take into account the individual objectives, financial situation, risk tolerance, or specific circumstances of any particular investor. Investment decisions should be made in consultation with a qualified advisor based on a comprehensive assessment of the investor’s individual circumstances.

Sources are believed to be reliable; however, their accuracy and completeness cannot be guaranteed.

Regards,

Kinsted Wealth