Make the Most of your Energy Equity

Commentary • Education

Date posted

Jun 9, 2026

When markets reward you, it's easy to conflate performance with prudence. Your company's stock is working. You understand the sector better than almost anyone. All of that is true — and none of it changes the fact that having the majority of your personal wealth tied to a single company in a single commodity-linked industry is a financial vulnerability, not a strategy.

At Kinsted, we work with high-net-worth individuals, families, and executives across Western Canada. We see this pattern frequently among energy executives: a portfolio that has grown substantially on paper, concentrated in company equity, with income, bonus, and job security all drawn from the same source. The next step isn't to abandon your position, it's to think clearly about what you actually own, and what a thoughtful path forward looks like.

Here are three things we'd encourage you to be doing right now.

Honestly audit how concentrated you actually are

Most executives significantly underestimate their concentration. That's because the math is counterintuitive when things are going well. Your company stock has gone up, which means it now represents a larger share of your net worth than it did twelve months ago, often without you having done anything at all.

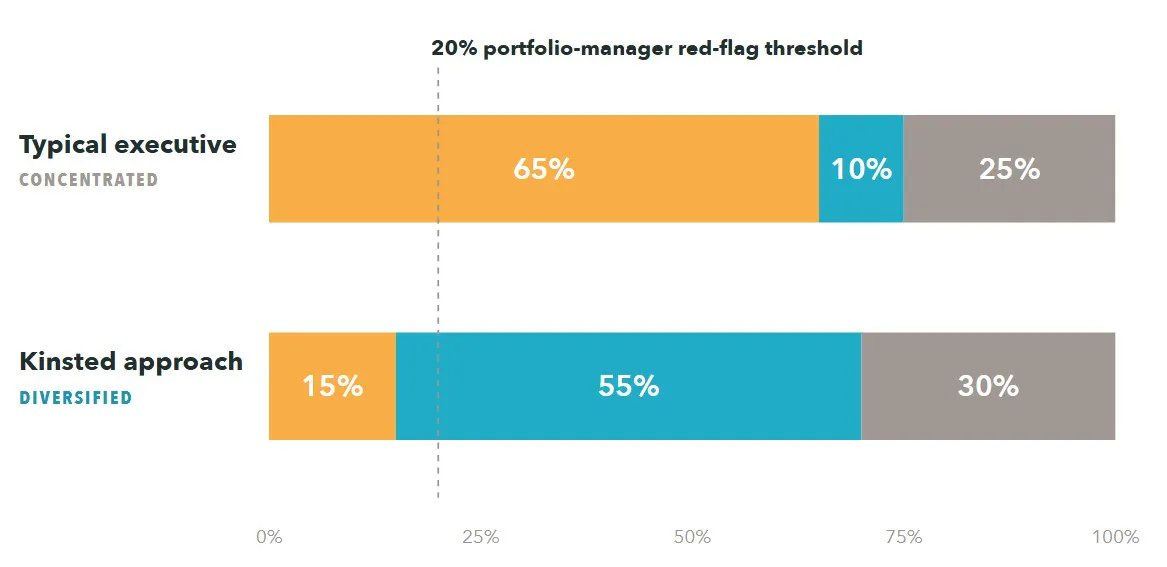

A proper concentration audit means adding up not just your vested shares, but your unvested RSUs at current value, your in-the-money stock options, any deferred compensation tied to company performance, and your ESPP holdings. Then compare that total to your entire investable asset base. According to industry research, most portfolio managers raise a red flag when a single security exceeds 10–20% of investable assets. At 30% or above, concentration becomes a dominant planning issue. Many of the energy executives we speak with discover they're considerably above that threshold, concentrations of 50–80% are not unusual in this situation.

Figure 1: Net-worth Composition - the energy executive's portfolio, before and after.

Disclaimer: Illustrative composition based on Kinsted client patterns; thresholds reflect industry guidance.

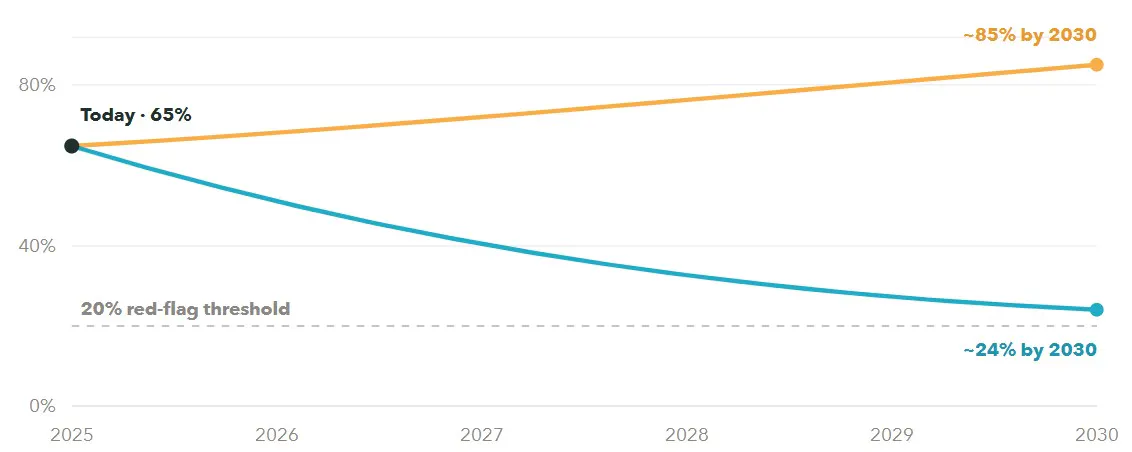

Concentration is not a point-in-time number you can check once and forget. It is a trajectory. Every vesting event adds more company stock, every new grant layers on more, and, in a strong market — appreciation quietly inflates the position faster than the rest of your net worth can keep up. Do nothing, and you don't simply stay concentrated; you become more concentrated with every passing year. The right question isn't “how concentrated am I today?” but “where does this end up in three, five, ten years if I keep doing what I'm doing?”

Figure 2: The Trajectory - Concentration Compounds, Unless You Act On It

Now add the less obvious layer: your salary, your bonus, your future grants, and your career trajectory are all tied to the same company and the same commodity cycle. When oil prices fall, they don't just affect your stock, they affect everything simultaneously. That correlation is the real risk, and it doesn't show up on a standard brokerage statement.

- 40% of all Russell 3000 stocks since 1980 suffered a permanent 70%+ decline from peak — with little to no recovery

- 67% of individual stocks underperformed the Russell 3000 index over their lifetime.

- >40% catastrophic loss rate is higher in the energy sector (Metals & Mining) than the broad market average.

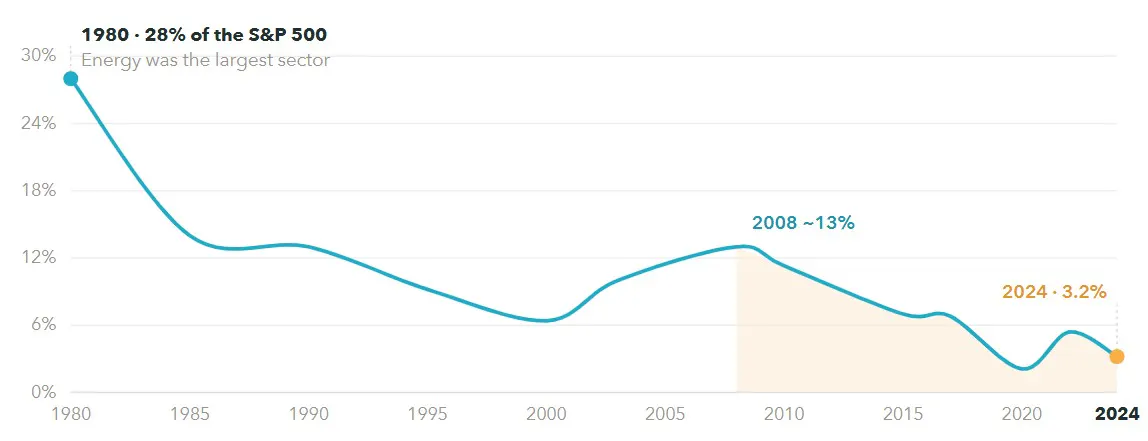

That last data point is worth sitting with. J.P. Morgan's landmark research, which analyzed over 13,000 stocks across four decades — found that the energy sector specifically sees a higher rate of catastrophic, non-recovering stock declines than the market. This isn't an indictment of oil and gas as an industry. It is a reminder that commodity cycles are real, and that even well-run companies in strong sectors are not exempt from them.

Build a systematic, tax-aware plan for selling into strength

Waiting is a mistake. Executives wait for the stock to hit a round number. They wait for the next quarter. They wait because selling feels like a statement about their confidence in the company or the sector. Meanwhile, concentration compounds and embedded tax liability grows.

The counterintuitive truth: a strong stock price is the best time to diversify, not the worst. You have more capital to redeploy, a clearer picture of your realized gain, and you are acting from a position of choice rather than necessity.

This matters more than many executives realize. In the oil and gas sector specifically, equity compensation has grown substantially in recent years. According to Pay Governance's 2025 compensation study, long-term incentive values for oil and gas CEOs grew by a median of nearly 8% year-over-year, with certain sub-sectors seeing increases well above that. For E&P executives, annual bonus payouts reached a median of 142% of target — reflecting how well the sector has performed. That is a lot of new equity entering portfolios that may already be concentrated.

- 142% Median annual bonus as a percentage of target for E&P CEOs in 2024 — reflecting strong sector performance.

- 98% of long-term incentive awards in oil & gas are now RSUs or performance share units — all delivered as company stock.

Rather than making ad hoc decisions at vesting, work with your portfolio manager to build a structured selling plan that accounts for your vesting schedule, your other income events (bonus payments, option exercises), and your marginal tax rate in Alberta. In Canada, 50% of capital gains are included in taxable income — so the timing and sequencing of dispositions across calendar years matters considerably. A plan that sells across two or three tax years can produce materially different after-tax outcomes than one that liquidates everything in a single quarter.

For executives with significant unvested equity, the planning conversation also needs to include what happens if you leave the company, are acquired, or face a commodity-driven market correction — scenarios where your options around timing and volume can become constrained very quickly.

Planning ahead — not reacting at vesting — is what creates real optionality.

Deploy the proceeds with the same institutional discipline your pension fund uses

This is the part that gets skipped. An executive sells a block of shares — often a meaningful amount of capital, and then the proceeds sit in cash, or get invested reactively into something that doesn't account for what they're actually trying to accomplish.

At Kinsted, this is the work we find most meaningful. When we receive proceeds from equity diversification, we don't slot them into an off-the-shelf portfolio. We ask what role this capital needs to play in the context of your complete financial picture: your remaining company equity, your real estate, your business interests if applicable, your timeline, and your income needs. The goal is a portfolio that doesn't simply move in lockstep with your company's share price or the price of a barrel of oil.

Figure 3: Energy's share of the S&P 500, four and a half decades

Disclaimer: Sector classifications evolve; figures rounded for visual clarity. — S&P Dow Jones Indices · Sector weights

Investing Alongside The Institutions

Our investment approach is built around the principle that private clients deserve access to the same strategies and asset classes that institutional investors — pension funds, endowments, sovereign wealth funds — have long used to protect and grow capital. That means genuine diversification across asset classes: public equities managed without the conflicts of large institutions, private credit, real assets, and alternatives that don't simply replicate the risk profile you're trying to move away from.

For many Calgary energy executives we work with, this conversation is the first time someone has looked at their full financial picture — equity compensation, real estate, pension entitlements, tax situation, estate structure — in an integrated way. That integration is what transforms a collection of accounts into an actual financial plan.

The Honest Case for Acting Now

We're not suggesting that oil and gas is in trouble, or that your company isn't a well-run business. We're suggesting that even well-run businesses in strong industries go through cycles — and that the correct time to prepare for those cycles is not when they arrive.

The research on this is consistent and clear. J.P. Morgan's analysis of 13,000 companies across four decades found that two-thirds of individual stocks underperform a simple broad market index over their lifetime — and that the energy sector is among those with the highest rates of permanent, non-recovering losses. That data doesn't come from a bearish view on oil. It comes from studying what actually happens to individual stocks over long periods of time.

The energy executives who tend to be in the strongest financial position over the long run are not the ones who held the most company stock for the longest period. They're the ones who recognized that their career, their income, and their equity were already a substantial bet on their sector, and who deliberately built a financial life around something more durable than any single company or commodity price.

Diversification from a position of strength is an act of confidence, not doubt. It says: I've built something real here, and now I'm going to protect it properly.

The Bottom Line

This is what Kinsted does best.

We work with energy executives and other high-net-worth clients across Western Canada who have meaningful equity compensation and want to think clearly about what comes next. We're independent, fee-based, and we don't benefit from keeping your money in any particular place. If this conversation resonates, we'd welcome the chance to sit down with you.

Important Disclosures

Disclaimer. This article is provided for general informational and educational purposes only and reflects the views of Kinsted Wealth as of the date of publication, which are subject to change without notice. It does not constitute investment, financial, tax, accounting, or legal advice, nor a recommendation, offer, or solicitation to buy or sell any security or to adopt any investment strategy. Nothing herein should be relied upon as the basis for any financial decision, and reading this article does not create an advisory or client relationship with Kinsted Wealth. Every individual's circumstances differ; you should consult your own qualified portfolio manager, tax advisor, and legal counsel before acting on any information contained here.

Forward-looking and hypothetical information. Certain figures, charts, and scenarios in this article — including any projections of future portfolio concentration, asset values, or market conditions — are hypothetical and illustrative only. They are intended to demonstrate general concepts, do not represent the actual results of any client, account, or investment, and are not a guarantee or prediction of future outcomes. Actual results will vary, potentially materially. Forward-looking statements involve known and unknown risks and uncertainties, and undue reliance should not be placed on them. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results.

Third-party data. Statistical references to J.P. Morgan Asset Management refer to its published "The Agony & the Ecstasy" analysis of Russell 3000 constituents (1980–2014); compensation data is sourced from Pay Governance's 2025 Oil & Gas Executive Compensation study; commodity and sector figures reference U.S. Energy Information Administration, ICE, and S&P Dow Jones Indices data. Information obtained from third-party sources is believed to be reliable but has not been independently verified, and its accuracy and completeness are not guaranteed. Tax commentary reflects rules in effect as of the date of publication and is general in nature; tax legislation and rates are subject to change.

Regards,

Kinsted Wealth